Vietnam’s tourism industry has experienced a strong post-pandemic recovery, with a significant increase in international arrivals. According to the General Statistics Office of Vietnam, in 2024, Vietnam welcomed 17.5 million international visitors, marking a 39.5% increase from the previous year and achieving the initial target of 17-18 million arrivals.

Among the key contributors to this growth, South Korea and Taiwan are among Vietnam’s three largest source markets, alongside China. Despite their high numbers of visitors, travelers from South Korea and Taiwan report the lowest satisfaction levels with their experiences in Vietnam, as reflected by their Net Promoter Scores (NPS) and Vietnam’s Destination Brand Strength Score (DBSS). This poses an important question: What accounts for this discrepancy, and how can Vietnam enhance its appeal to these travelers?

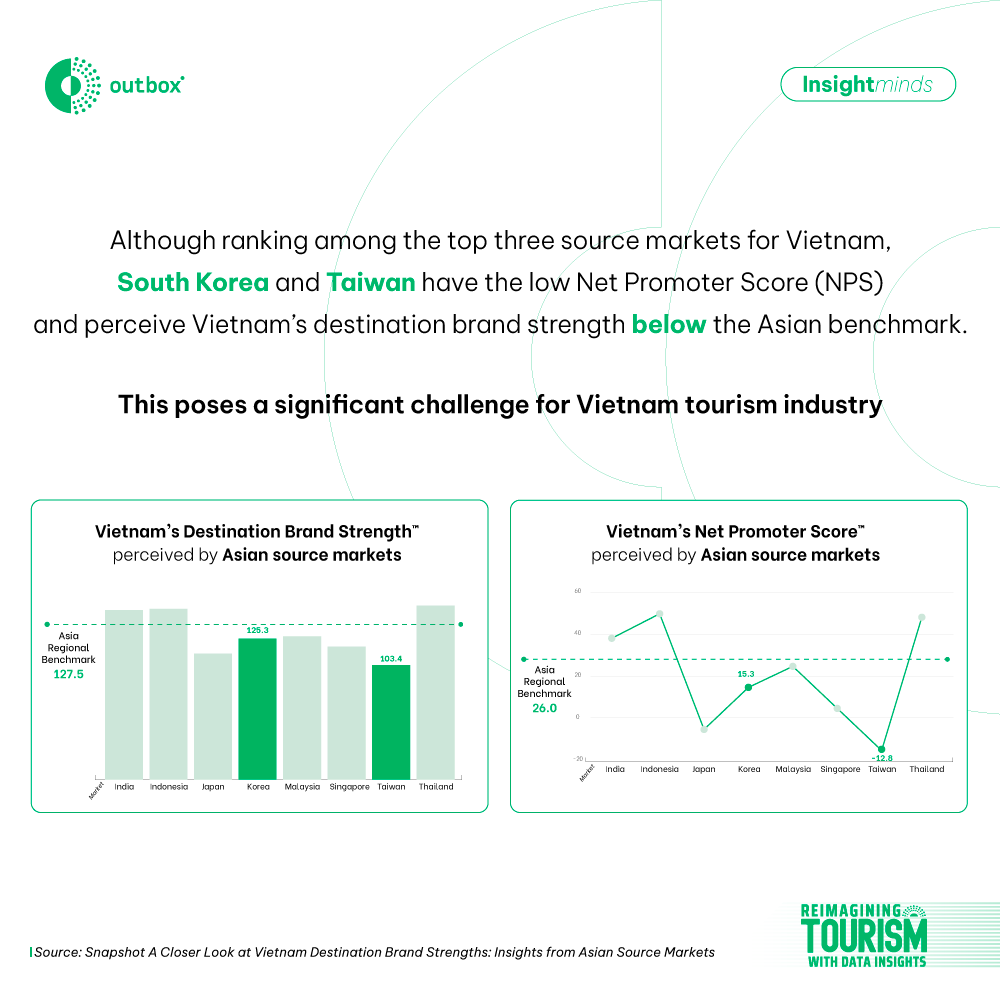

The Discrepancy: High Volume, Low Satisfaction

The Discrepancy: High Volume, Low Satisfaction

South Korea and Taiwan are among Vietnam’s top three source markets, contributing significantly to inbound tourism. In 2024, Vietnam welcomed approximately 4.5 million South Korean visitors (25.98% of total international arrivals) and 1.29 million Taiwanese visitors, reinforcing their status as key drivers of Vietnam’s tourism economy. Their substantial share of total arrivals underscores their importance, making it critical to understand and address their perceptions of Vietnam as a travel destination.

Despite their large market sizes, travelers from South Korea and Taiwan have relatively low brand perception and satisfaction regarding Vietnam as a destination. The Destination Brand Strength (DBS) score for South Korea is 123.5, while Taiwan travelers report the lowest DBS score for Vietnam at 103.4, which is also the weakest compared to their perceptions of other Southeast Asian destinations. When benchmarked against the Asia average of 127.5, both South Korea and Taiwan fall short, reinforcing the notion that Vietnam’s destination branding is weak in these markets.

More concerning is the Net Promoter Score (NPS), which measures travelers’ likelihood to recommend Vietnam. The NPS for South Korean visitors is only 15.3, while Taiwan stands at -12.8, the lowest among all surveyed Asian source markets. This sharply contrasts with the Asia benchmark NPS of 26, indicating that despite high visitation numbers, travelers from these countries are less likely to recommend Vietnam as a preferred destination. For Taiwan, the negative Net Promoter Score (NPS) of -12.8 indicates that most travelers do not recommend Vietnam as a destination. In fact, many may share negative experiences, which could harm the country’s image in this market. As a result, Vietnam risks losing the opportunity to attract both first-time and repeat visitors from Taiwan, as these travelers not only rarely recommend the destination but may also communicate unfavorable impressions.

Interestingly, the issue does not appear to stem from a lack of destination marketing efforts. The Destination Marketing Exposure (DME), which assesses the visibility of Vietnam’s tourism marketing in different countries, is relatively high for both South Korea and Taiwan. According to Outbox’s survey, Vietnam’s DME score in these countries is among the highest in the region, suggesting that awareness and exposure are not the primary barriers to improving satisfaction. Instead, the low NPS and DBS scores may reflect deeper structural issues, such as service quality, infrastructure, or a misalignment between experiences offered and traveler expectations.

Understanding the Challenges Behind Low Satisfaction

Given these insights, it is essential to examine the factors contributing to visitor dissatisfaction. Several reasons could explain why South Korean and Taiwanese travelers, despite their large numbers, report lower satisfaction with their experiences in Vietnam. For instance, these travelers may experience a gap between their expectations and the reality they encounter. High expectations for service quality, convenience, and infrastructure may not always be met, leading to lower satisfaction levels.

Additionally, competition from other Asian destinations plays a role; Vietnam may not differentiate itself enough to encourage repeat visits. Language barriers and inconsistent service quality can further impact the visitor experience, as Korean and Mandarin-speaking travelers might struggle with communication in Vietnam. Moreover, the tourism infrastructure, such as airport efficiency and local transportation, may not fully meet the needs of these high-volume visitors, resulting in logistical frustrations and negative word-of-mouth.

To improve satisfaction levels, Vietnam needs to enhance the visitor experience across multiple aspects. Service quality must be elevated through better hospitality training and multilingual support. Improvements in tourism infrastructure, including transportation and signage in Korean and Chinese, are essential to ensure convenience. Furthermore, Vietnam’s tourism offerings should be tailored to better align with South Korean and Taiwanese preferences, particularly regarding food, shopping, and entertainment. Beyond exposure, destination branding must emphasize unique experiences that set Vietnam apart from its regional competitors. By addressing these gaps, Vietnam can convert high visitor numbers into stronger advocacy and encourage repeat travel.

Conclusion

South Korea and Taiwan are essential to Vietnam’s inbound tourism; however, the lower satisfaction levels reported from these markets indicate an area that requires improvement. Although destination marketing efforts have successfully increased visibility, Vietnam must now concentrate on enhancing visitor experiences to transform high visitor numbers into positive word-of-mouth and repeat travel. Key steps to elevate Vietnam’s appeal and ensure long-term growth in these important markets include addressing service gaps, refining branding, and strengthening tourism infrastructure.